Debt: Borrowing money in times of Economic Contraction

When my kids were younger they used to play a game in which everything they said was turned opposite. Up was down, hot was cold, yes was no.

As we enter a contracting economy, virtually every assumption and expectation we have held about the grow-grow-grow economy is turned opposite. What was trending up is now down, investments that were hot are now cold. Advice that was good is now bad. “Yes, do it” has now become “no way.” The presumptions of leveraging and debt are similarly reversed.

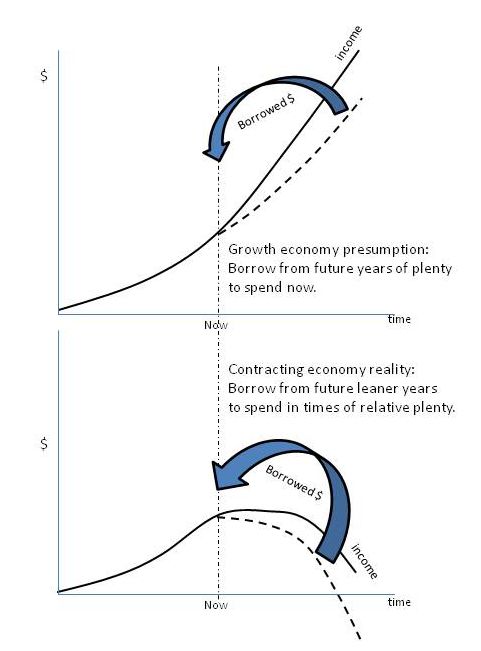

Debt is a concept which very much belongs to a growing economy. When you borrow money, you presume that in the future you will be earning enough to live on plus repay your debt plus interest. In a growing economy, this isn’t too tough to imagine. You are, in essence, borrowing from future plenty to consume part of that plenty now in leaner times.

In a contracting economy, this idea is turned upside down. When you go to borrow from the future, that future now represents leaner times. Things in the present are relatively more abundant! Borrowing in a contracting economy means taking from leaner times to consume in times of relative plenty.

In a contracting economy, if your income remains steady (i.e. not growing, but not decreasing either) your obligation to repay loan-plus-interest means you will have less cash flow to meet your usual expenses. If you weren’t saving before — weren’t experiencing some surplus each month — then you will find that debt service means you can no longer meet your same, ongoing expenses. If your income is rendered unsteady, or it begins to decrease, it’s bad news: suddenly you no longer have enough for your regular ongoing expenses AND you have loan to replay PLUS interest. Debt completely hastens the decline.

It gets worse … If your typical monthly expenses are now increasing because peak oil is driving gas prices up, increased transportation costs are driving consumer goods up, climate-issues-plus-petroleum-costs are driving food costs up … you’re in a world of hurt. In a contracting economy, debt no longer makes sense.

If you cannot meet expenses and you’re in a contracting economy, you simply have no alternative but to cut expenses. (How? see resources below)

It’s important to view these statements within a historical perspective: our views of loans and debt weren’t always this way. Easy credit over the past 30-50 years of extreme growth has warped our perspective. Right now we expect that getting a loan will “help us out” and those in the business of lending perpetuate this myth.

But prior to the 1940s people had a very different attitude about taking on debt. They saved up and bought large items for cash. Or they used (interest-free) layaway, which really was just a supervised savings program. If they did turn to a lender it was for very short term and rather low rates. None of the 15-20% we see in today’s credit cards. Many homes were bought outright. At most, home financing terms for those who did use them were more like 50% down and a 5 year mortgage. All of this is to say that the attitudes we have embraced in recent decades are the attitudes that fit with an economy which is in exponential growth mode.

But we are no longer in such an economy (explanation) We are now in economic contraction and our views of debt, credit cards, car loans, college loans, mortgages, business lines of credit, venture capital, government assuming debt, government issuing school bonds, must evolve to match this changed landscape. In this new, contracting world, debt doesn’t make sense.

This post was updated May 6, 2021.

- Why interest-free? See “Robbing Peter to Pay Paul” chapter in Sacred Economics, by Charles Eisenstein, http://charleseisenstein.com/online-text/

- More about “Debt and the Transition Economy” http://transitionus.org/blog/debt-and-transition-economy

- How does a current economic method of creating money via debt drive eternal growth? see Charles Eisenstein, Sacred Economics, chapter 6. at the subheading “An Economic Parable”

- Basics on how to budget: Check out the books of Tiffany Aliche, The One-Week Budget, and Get Good With Money. Although Aliche does not acknowledge this concept of a contracting economy, her basic tools will help you gain financial resilience.